Which is Better a 15 Year Fixed Mortgage or a 30?

Choosing between a 15-year mortgage or a 30-year mortgage requires a diligent review of the pros and cons of each and how they relate your individual goals/needs. Taking the time to research this before seeking a loan package can help ensure that you plan mortgage repayment in a way that will most benefit your future financial health. If you need help understanding what the pros and cons are of each, read on!

Choosing between a 15-year mortgage or a 30-year mortgage requires a diligent review of the pros and cons of each and how they relate your individual goals/needs. Taking the time to research this before seeking a loan package can help ensure that you plan mortgage repayment in a way that will most benefit your future financial health. If you need help understanding what the pros and cons are of each, read on!

Advantages of 15-Year Mortgage Loans

Believe it or not, but a 15-year mortgage loan is classified as a “short-term” loan. This shorter loan period will offer you the following benefits. (We will discuss each in depth).

- Pay Lower Interest Over the Life of the Loan

- Build Equity More Quickly

- Avoid Negative Equity

Pay Lower Interest Over the Life of the Loan

If you are able to qualify for a 15-year mortgage, one of the major benefits is that you can get your debt eliminated more quickly with a shorter loan term. Not only that, you will save more money because borrowers can secure a lower interest rate with a shorter-term loan.

By being able to pay down the principal balance more quickly, and should you need to refinance, you will have a lower loan-to-value ratio which will make that process easier for you.

According to NerdWallet, a lower interest rate means lenders are taking on fewer years of risk so they can give borrowers lower interest rates. “That could mean, depending on the institution, a rate that’s anywhere from a half percent to three-quarters of a percent lower than for a 30-year, fixed-rate mortgage,” says Carlos Miramontez, vice president of mortgage lending at Orange County’s Credit Union.”

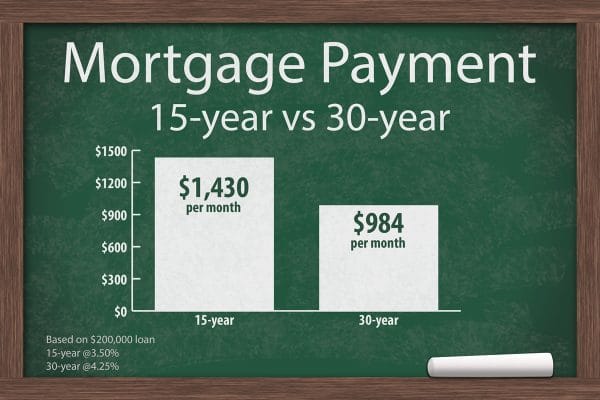

This lower interest rate could mean mega savings if you can qualify. Nerd Wallet’s data shows the following savings, comparing a $250,000 home purchase with a 15-year mortgage and a lower interest rate compared to a 30-year mortgage:

“A 30-year fixed-rate mortgage at 3.88% has monthly payments of $1,176 and a total interest cost of $173,471. A 15-year fixed-rate mortgage at 3.19% has monthly payments of $1,749 and a total interest cost of $64,890 — a savings of $108,581 if you kept the loans for their entire terms.”

Build Equity More Quickly

One of the chief benefits of homeownership is the equity you build. This equity becomes a major asset that can then be used for a variety of situations and needs. When you sell the home the value you sell it for becomes cash in your pocket. Equity is a home is also something you can borrow against with a home equity loan or a home equity line of credit. Often, homeowners will roll their equity into their next home purchase, using it as a down payment so that they can enjoy lower mortgage payments and interest.

15-year mortgage terms require higher payments each month, yes, but that means that you are building equity more quickly too. Equity increases as your debt decreases. (Equity also increases if the market value of your home increases so always stay-up-to-date on current market trends.)

Avoid Negative Equity

Being able to pay off your home more quickly can help you avoid negative equity, or being “upside down” on a house. Making larger payments means you’re establishing equity in the property more rapidly, decreasing the likelihood that you will be affected by negative equity if home values fall.

Home loans that reach a point where the loan amount is higher than the market value of your home, can lead to borrower distress. While it is almost impossible to predict when a certain housing market or demographic is going to decline, there are steps you can take to help avoid it so you make smarter, more informed financing decisions.

Disadvantages of 15-Year Mortgage Loans

While there are some great pros to the 15-year mortgage loan, there are some cons to consider that might make you change your mind:

- Monthly mortgage rates will be higher.

- Higher mortgage payments means less money for other priorities.

- More risk of loan foreclosure or default

Monthly Mortgage Rates Will Be Higher

A big factor to consider when researching 15-year mortgages is if you can afford the monthly payment– it will be significantly larger on a 15-year loan than a 30 year one. (For example, a $250,000 mortgage at today’s national rates of 5.26 percent for a 30-year fixed-rate loan vs. 4.78 percent for a 15-year one would result in:

- Monthly payments: $1,948 vs. $1,382 = $566 per month more for the 15-year loan

- Total payments: $350,721 vs. $497,540 = $146,819 more over the life of the 30-year loan

- Total interest paid: $100,721 vs. $247,540 = $146,819 more over the life of the 30-year loan

In this example, monthly payments on the 15-year loan are more than 40 percent higher than the 30-year loan. But, your TOTAL payments over the life of the loan are almost 30 percent less, yielding a savings of almost $147,000.

Higher Mortgage Payments Means Less Money for Other Priorities

The risky component with 15-year mortgages is they can leave you in a vulnerable position. With a large portion of your budget tied up in your monthly mortgage payment, when unplanned circumstances hit, you could find yourself in a tight spot. Loss of income, medical costs, additional children etc., could change your monthly income causing strain on your budget. A higher mortgage could also keep you from saving more for retirement.

A safer alternative may be to make additional monthly payments on a 30-year mortgage when you can. Most loans will allow you to do this without a penalty.

More Risk of Loan Foreclosure or Default

Like was mentioned above, borrowers with high monthly mortgage payments run the risk of not being able to pay them if financial circumstances change.

Before entering into a 15-year mortgage, talk through your financial situation and goals with a professional financial advisor to make sure you have a clear perspective of your best options.

How Do You Know If a 15-Year Mortgage is for You?

According to Credit.com, a 15-year mortgage may be a viable option for you if:

- You don’t want debt hanging over you into the future

- You have a strong income

- You expect to see an increase in income fairly soon

- You expect a decrease in debt soon

- You plan to retire in less than 30 years